Answer:

Section 17(2)(vi) covers perquisites as prescribed by the Board (CBDT). The prescribed perquisites under Rule 3 cover:

- Accommodation (Rule 3(1))

- Motor car (Rule 3(2))

- Other movable assets (Rule 3(7))

Transfer of immovable property at concessional rate is NOT specifically prescribed under Rule 3

Conclusion — Employee’s Tax Implications

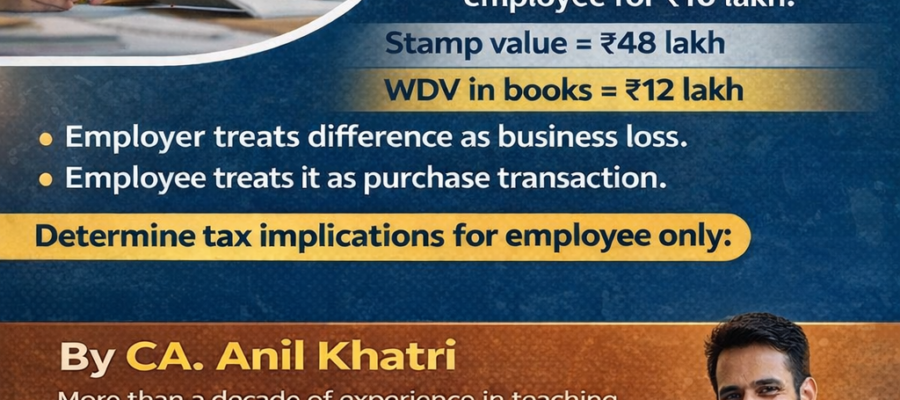

Head of Income: The ₹38 lakh differential (₹48L stamp value − ₹10L paid) is taxable as Salary under Section 17(2) as a perquisite. Section 56(2)(x) does not apply since Salary head takes precedence.

Quantum of Tax: ₹38 lakh added to gross salary and taxed at applicable slab rates. Employer must deduct TDS under Section 192.

Cost of Acquisition (future sale): ₹48 lakh (₹10L paid + ₹38L already taxed as salary) to avoid double taxation.