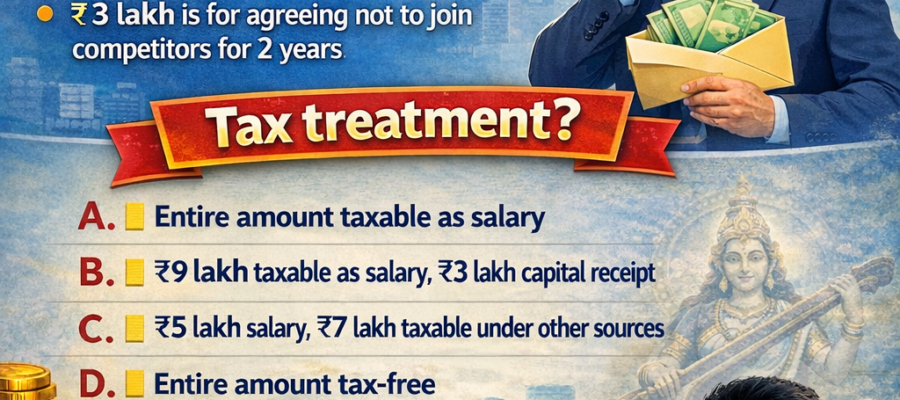

Tax Quiz Answer

The correct answer is B. ₹9 lakh taxable as salary, ₹3 lakh capital receipt

Here’s the reasoning under Indian Income Tax law:

₹4 lakh – Compensation for loss of job Taxable as profits in lieu of salary under Section 17(3) → taxable as salary

₹5 lakh – Unpaid salary arrears This is clearly salary income → taxable as salary

So ₹4L + ₹5L = ₹9 lakh taxable as salary

₹3 lakh – Non-compete agreement (not to join competitors for 2 years) This is received for restricting a future right/activity. Under Indian tax law, non-compete fees received as a one-time capital receipt (not in the course of business) are treated as a capital receipt, and since it doesn’t fall under any specific head of income in this context, it may be treated as a capital receipt not chargeable to tax (or taxable as capital gains depending on facts).

For exam purposes (CA/CMA), this is classically treated as a capital receipt → not taxable as salary.